Interest rates and inflation are often linked and tend to be inversely correlated. Inflation refers to the rate at which prices for goods and services rise. The interest rate is the amount charged by a lender to borrow money. Interest rates are based on the Federal Funds rate set by the Federal Reserve, also referred to as the Fed. The Fed controls short-term interest rates. It increases or decreases the rate based on how the economy is doing. The Fed attempts to influence the rate of inflation by setting and adjusting the Federal Funds rate. The Fed Funds rate is the target interest rate set by the Fed and is the rate at which commercial banks borrower and lend their excess reserves to each other. This rate influences short-term rates on consumer loans and credit cards. Mortgage rates are not set by the Fed, but typically move in the same direction as the Fed Funds rate.

In general, people borrow more money when interest rates are low. More capital translates into more spending by businesses and individuals. This causes the economy to grow and inflation to increase. When the nation shut down in 2020 to stop the spread of coronavirus, the Fed jumped into action, and cut the Fed Funds rate to zero, to encourage spending. The action of the Fed ultimately led to record low mortgage rates and a boom in refinancing. American homeowners who refinanced their mortgage benefitted greatly from lower interest rates.

But what happens when the Fed increases the Fed Funds rate? Rising interest rates encourage people to save more, because their savings will accrue at a higher rate of interest. If more money is saved rather than spent, the economy slows and inflation should decrease.

The justification for a rate hike now seems to be that cheap credit allowed spending to overrun the economy’s ability to produce what people want to buy. With credit-fueled demand exceeding supply, prices are rising quickly. By increasing short-term rates, the Fed hopes to slow the economy by making it more expensive for businesses and consumers to borrow money. In an effort to combat inflation, the Fed is expected to raise rates multiple times this year beginning in March.

How does this affect mortgage interest rates? The central bank has been the biggest buyer of mortgage-backed securities since the start of the pandemic. It is now winding down its purchases and trying to shrink the $2.7 trillion stockpile it has built up. These pools of home loans, hot investments for much of the pandemic, are now selling off and the result is higher interest rates on mortgages.

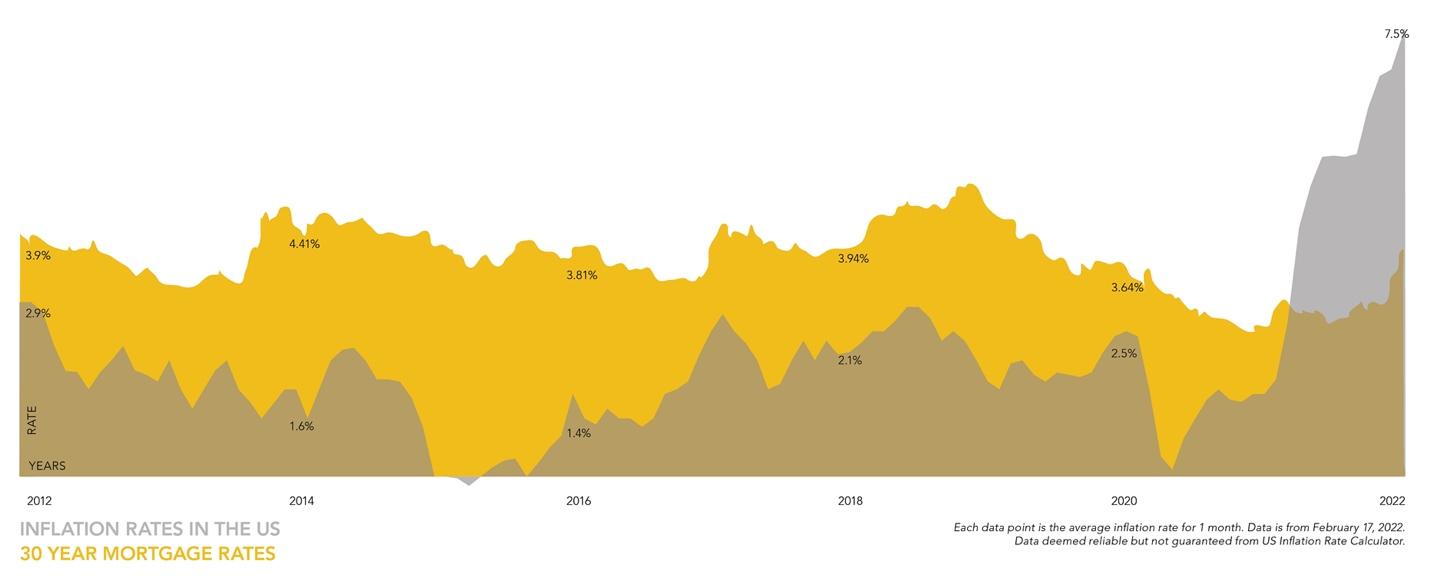

The turbulence in mortgage bond market affects households in a direct manner. Less demand for mortgage bonds means issuers must offer higher yields to attract investors. Lenders then have to increase interest rates on the mortgages inside those bonds. Already, the rate for a 30-year fixed mortgage is around its highest level since the beginning of the pandemic. Mortgage rates are on the rise, though they still remain incredibly attractive from a historical perspective. Active homebuyers seeking properties today will reap the benefits of the historically low interest rates! Don’t put off buying a home! Contact your Fazendin Realtor® today to get started.

New Loan Limits for 2022

In other mortgage news, the Federal Housing Finance Authority (FHFA) announced new conforming loan amounts for 2022, which increased from $548,250 in 2021 to $647,200 for one-unit homes. Likewise, the U.S. Department of Housing and Urban Development (HUD) announced new FHA loan limits of $448,500 for properties located in the metro area and $420,680 outside the metro area. This is great news for many homebuyers in Minnesota.

For more information or to take advantage of the low interest rates, please contact Donnie Robin.

Donnie Robin

Loan Officer NMLS #1062202

612.751.5653

Donnie(at)DonnieRobin(dotted)com

www.DonnieRobin.com